The "Invisible" Price Tag: 5 Surprising Truths About Buying a Home in Texas

First-time buyers often walk into a trap, fixating on a single number: the down payment. While a 3% or 5% entry point is a significant achievement, it is rarely the finish line for your capital allocation. In the competitive Texas market, a $400,000 home requires far more liquidity than the initial "sticker price" suggests. To navigate this landscape as a strategist rather than a spectator, you must understand the "cash to close" reality and the sophisticated levers available to protect your reserves.

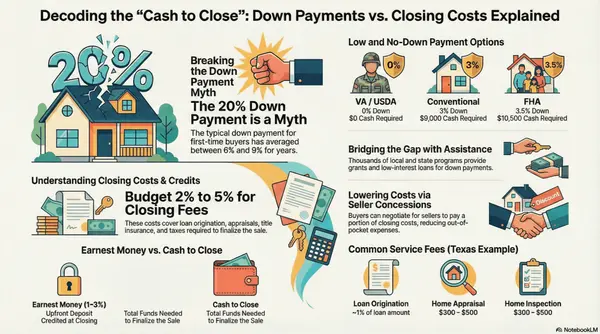

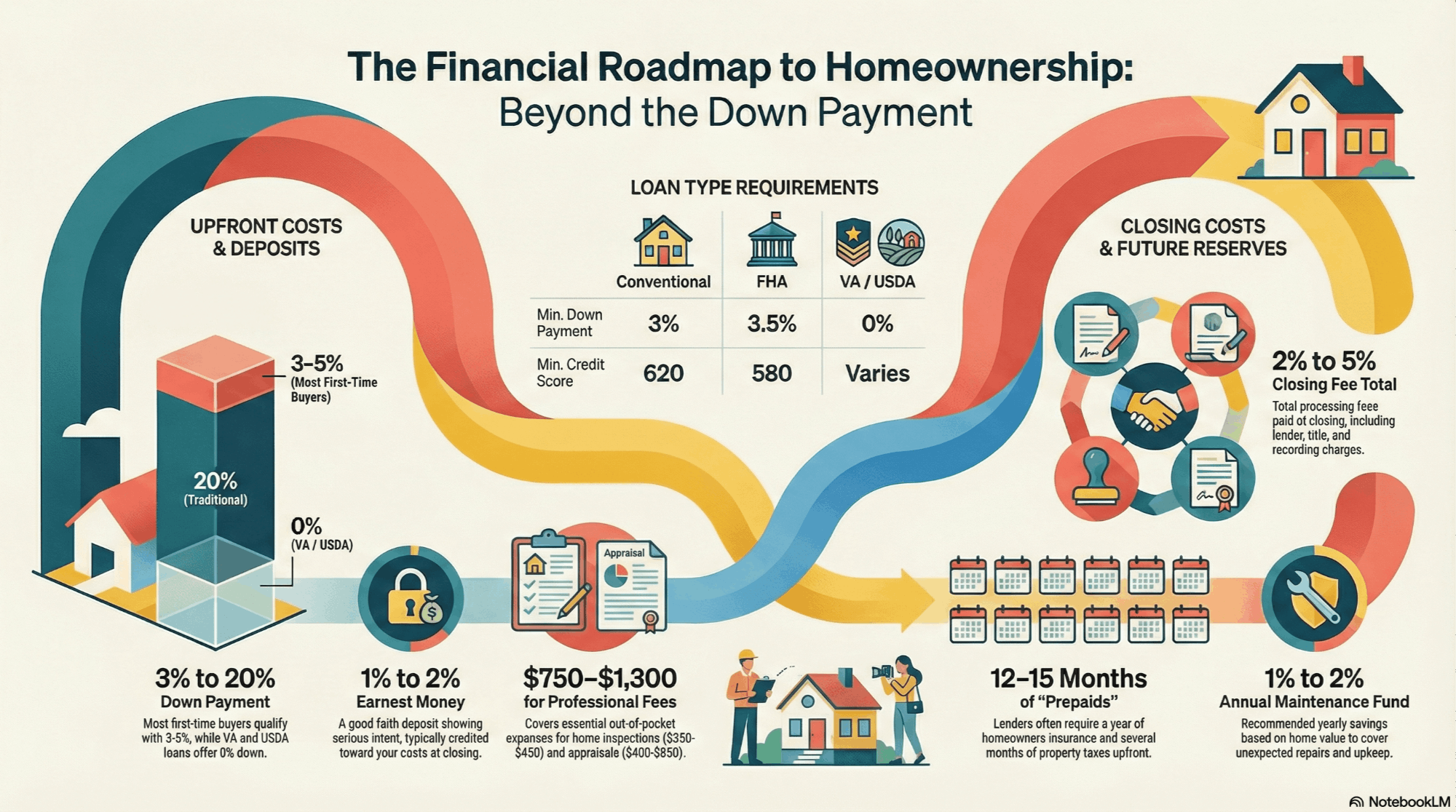

1. The "Total Cash" Reality: Why 3% Down Isn't Enough

The most common failure in a buyer’s financial planning is conflating the down payment with the total liquidity required at the closing table. While loan programs exist for as little as 3% down, transaction costs—the professional fees and taxes required to finalize the debt—create a significant capital gap.

In Texas, closing costs typically range from 2% to 5% of your mortgage loan amount. This includes high-stakes line items like title insurance, loan origination fees, and appraisals (which generally run between $400 and $850). When these are layered on top of your down payment, your total cash requirement shifts from a manageable percentage to a substantial burden.

As real estate strategist Scotty Gifford notes:

"Closing costs usually range from 2% to 5% of the price of your mortgage loan amount... which can then increase the total amount of cash needed to closer to 7%–9% of the purchase price."

2. The "Roll-In" Strategy: Using Seller Concessions as a Financial Lever

If your primary objective is capital preservation, you should view "Seller Concessions" as a strategic financial lever. This maneuver involves negotiating a higher sales price paired with a corresponding seller credit to cover your closing costs, effectively "rolling" those transaction fees into the long-term loan.

This is a sophisticated play for liquidity management, but it is governed by strict regulatory limits based on your loan type and down payment:

- Conventional Loans (Primary Residence):

- Less than 10% down: 3% limit

- 10%–24.9% down: 6% limit

- 25% or more down: 9% limit

- FHA Loans: 6% limit

- VA Loans: 4% limit

- USDA Loans: 6% limit

- Investment Properties: 2% limit

The Strategy in Action: The "Joe Buyer" Lever Consider a home listed for $300,000. "Joe Buyer" could offer $297,000 with no assistance, or he could offer the full $300,000 but request $3,000 in seller concessions. For the seller, the net proceeds are identical. For Joe, he preserves $3,000 in immediate cash. While this increases his monthly obligation by approximately $17 to $18, the opportunity cost of that $3,000 in upfront liquidity often makes this the superior wealth-optimization move.

3. The Escrow Escape: The Arbitrage of Managing Your Own Taxes

Once you’ve utilized concessions to preserve your liquidity, your next move is to ensure that your remaining capital isn't sitting dead in a bank’s interest-free vault. Most lenders require an "Escrow Account"—a padded reserve used to pay future property taxes and insurance. In Texas, lenders often demand up to four months of property taxes upfront to "pad" these accounts.

However, certain Texas-based lenders allow savvy borrowers to opt out of escrow entirely. This provides a unique opportunity for interest-rate arbitrage: instead of the bank holding your money, you retain those funds in a high-yield savings account, earning interest until the tax bill is actually due.

Reef Merhi of Texas United Mortgage explains the advantage of this consumer choice:

"With us, not only can you hold the money and make your payments at your discretion... but you get to choose how you use that money such as placing it in a high yields savings account until you're ready to make the payment."

4. The 3-Day Countdown: The High-Stakes Timing of Texas Contracts

In Texas, the "Effective Date" of a contract triggers a high-stakes, 72-hour execution window. Buyers must deliver both the Earnest Money (good-faith deposit) and the Option Fee to the Title Company within three days.

Precision is critical here. Per TREC rules updated in 2021, the Option Fee is no longer paid to the seller; it must be delivered to the Title Company. Furthermore, you must calculate the deadline with care: do not exclude weekends or holidays from the count. If the Effective Date is Thursday, Day 1 is Friday, Day 2 is Saturday, and the deadline is Monday (as the rule allows an extension to the next business day only if Day 3 falls on a weekend or legal holiday).

The Breakdown of Non-Negotiables:

- Earnest Money: Usually 1%–2% of the price. Refundable if you terminate for a cause allowed by the contract (e.g., financing failure).

- Option Fee: Generally around $100. This is non-refundable. It purchases your "Option Period" (typically 7–10 days), which is your exclusive window for due diligence and inspections.

5. The "Post-Closing" Budget: Why the 1% Rule is the Absolute Minimum

Closing day is not the finish line; it is the beginning of a long-term capital maintenance cycle. Strategists use the "1–2% Rule," earmarking 1% to 2% of the home's value annually for maintenance. For a $300,000 Texas home, that means budgeting $3,000 to $6,000 every year for the inevitable.

The "invisible" price tag of homeownership goes far beyond the mortgage. Data from Zillow and Thumbtack reveals that the average homeowner spends an additional $1,180 per month above their mortgage payment on utilities, property taxes, insurance, and essential maintenance.

To protect your equity, an emergency fund covering 3–6 months of living expenses is non-negotiable. Without it, a $1,500 water heater failure or a $10,000 HVAC replacement becomes a high-interest debt crisis rather than a routine maintenance event.

Conclusion: The Long Game of Homeownership

Buying a home in Texas is a complex financial maneuver that requires a transition from "saver" to "strategist." While the hidden costs—from title insurance and escrow padding to a $1,180 monthly maintenance average—are higher than they appear, the wealth-building potential of Texas real estate remains immense.

Now that you have decoded the true cost of the keys, the question remains: are you simply saving for a house, or are you executing a homeownership strategy?

Categories